Business trips are part of everyday life in many companies, from one-day customer meetings to conferences abroad lasting several days. But as soon as a business trip lasts longer than eight hours, special tax rules apply. For employees, the question arises: What per diems am I entitled to? And for finance teams, it's about how these travel expenses can be accounted for correctly, efficiently and in compliance with GoBD.

- Meal allowance from 8 h: €14/€28.

- Accommodation allowance: €20/night (domestic).

- Mileage allowance: €0.30/km (car).

- Reductions for meals provided.

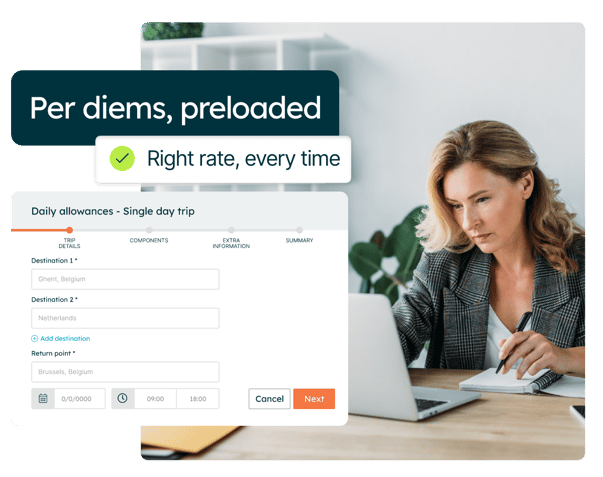

- Mobilexpense automates flat rates, receipts & GoBD-compliant processes.

In this article, you will get a comprehensive overview of the current per diems 2025, the most important special regulations, and learn how you can make your travel expense accounting more efficient with modern expense management software.

Why is the 8-hour rule so important?

The 8-hour rule is a key criterion in German travel expense law. It determines whether employees are entitled to a per diem meal allowance.

The background to this is that anyone who is on the road for several hours generally has higher expenses for meals, which are taken into account for tax purposes by means of lump sums.

Not every business trip automatically counts as a business trip. For tax purposes, a business-related away activity only exists if employees work outside their primary place of work and do not have a regular place of work there. The same principles therefore apply for one-day customer appointments or trade fair visits as for business trips lasting several days - the decisive factor is that the activity takes place away from the usual place of work.

However, numerous details must be taken into account to ensure that these flat rates are applied correctly: Arrival and departure days, reductions for meals provided or differences between domestic and international trips. In practice, mistakes are often made here - with consequences for the tax return or internal accounting.

Lump sum for meals:

Small lump sum vs. large lump sum

Anyone who spends more than 8 hours traveling on business is entitled to a per diem meal allowance:

- Small lump sum: If you are absent for between 8 and 24 hours, you areentitled to €14.

- Large lump sum: If you are absent for more than 24 hours, you are entitled to €28.

- Trips lasting several days: The small flat rate of €14 applies for arrival and departure days.

Update 2025: A planned increase in expenses as part of the Growth Opportunities Act was not implemented. The previous rates from 2023 therefore continue to apply.

There is a change for professional drivers in particular: the lump sum was increased from €9 per calendar day to €10 from January 1, 2025.

Note on trips abroad

Different per diems for meals apply to business trips abroad, which are published annually by the Federal Ministry of Finance (BMF). The amounts differ depending on the country - and sometimes even the city - as they are based on the respective cost of living.

An example:

For a 24-hour business trip to the Netherlands, the lump sum is 47 euros, while for Poland (depending on the destination), between 34 euros (Wroclaw) and 40 euros (Warsaw) is provided.

Reductions for meals

Often overlooked: If employees are provided with breakfast, lunch or dinner, the lump sum must be reduced accordingly.

Example:

Anna attends a one-day meeting in Berlin. She is traveling for nine hours and would be entitled to 14 euros. However, as lunch is provided by the organizer, her entitlement is reduced by 40 percent - leaving her with 8.40 euros.

Such calculations are prone to error if they are done manually.

With Mobilexpense, you save yourself this work: the system automatically takes all reductions into account so that invoices are always correct.

Accommodation allowance for trips lasting several days

In addition to meal costs, accommodation costs are usually also incurred on longer trips. Here, too, there are fixed flat rates:

- Germany: 20 euros per night (as of 2025)

- Abroad: Different flat rates apply depending on the destination country.

If actual hotel costs are higher, these can be reimbursed on presentation of an invoice.

In order for travel expenses to be recognized for tax purposes, the tax office requires complete proof - such as receipts, hotel bills, tickets or receipts.

Mobilexpense simplifies this process with digital receipt capture: employees simply photograph receipts with their smartphone and all documents are archived in compliance with GoBD. This eliminates the risk of losing receipts or overlooking formal requirements.

Even personal receipts - for example, if a receipt has been lost - can be recorded. They count as proof, but do not entitle you to deduct input tax as no VAT is shown.

Flat-rate mileage allowance: What are you entitled to?

Even if a journey takes less than eight hours, travel expenses can be reimbursed. The so-called mileage allowance applies if the private vehicle is used for business trips:

- Car: 0.30 euros per kilometer

- Motorcycle/moped: 0.20 euros per kilometer

These values apply to both domestic and international trips. Digital mileage logging makes billing easier, as the distances traveled are automatically documented and the corresponding amounts are calculated correctly.

Special regulations in the Federal Travel Expenses Act (BRKG)

There are many special regulations and requirements in the Federal Travel Expenses Act (BRKG). Important to know:

- Reductions: If meals are provided to you (e.g. by your employer or at seminars), the lump sum can be reduced.

- Three-month period: After three months at the same place of work, the per diem meal allowance no longer applies.

- No entitlement to daily allowance: If the distance between the business activity and your place of residence or your place of employment is short, the per diem allowance does not apply (in accordance with § 6, paragraph 1 BRKG).

A digital solution makes sense to ensure that invoices remain correct despite these details. Mobilexpense supports companies with a legally compliant expense report that automatically takes all requirements into account and documents them in accordance with GoBD.

Who pays the flat rates?

In principle, employees have the right to reimbursement of business-related travel expenses. This is regulated in § 670 of the German Civil Code (BGB):

"If the agent incurs expenses for the purpose of carrying out the assignment which he may consider necessary in the circumstances, the principal shall be obliged to reimburse them."

However, employers are not obliged to pay lump sums. If the employer does not pay them, employees can claim the amounts on their income tax return.

- Allowance: 1,230 euros per year (as of 2025)

- Amounts already paid by the employer are taken into account.

Travel expense report with Mobilexpense

Business trips not only mean additional work on the road, but also a considerable amount of accounting work afterwards. Declaree by Mobilexpense makes this process digital, fast and error-free:

- All fixed data stored automatically (current BMF flat rates, mileage and accommodation rates).

- Employees enter variable data directly in the app (destination, duration, meals).

- Automatic calculation of reimbursements - without manual intervention or Excel.

- Digital receipts: simply take a photo and upload.

- GoBD-compliant archiving: all documents are stored in an audit-proof manner.

The result: transparent, error-free and efficient travel expense reports that take the pressure off both employees and finance teams.

Conclusion: Travel expense accounting 2025 - simpler with digital solutions

The rules surrounding travel expenses are complex and error-prone. In 2025, the flat rates will hardly change - the real difference lies in the way companies deal with these rules.

Manual calculations quickly lead to errors and cost valuable time. With Mobilexpense, companies not only save time and effort, but also ensure that their travel expense reports are correct, efficient and GoBD-compliant.

On this page:

- Why is the 8-hour rule so important?

- Lump sum for meals: Small lump sum vs. large lump sum

- Note on trips abroad

- Reductions for meals

- Accommodation allowance for trips lasting several days

- Flat-rate mileage allowance: What are you entitled to?

- Special regulations in the Federal Travel Expenses Act (BRKG)

- Who pays the flat rates?

- Travel expense report with Mobilexpense

Share this

5 Signs You Need an Alternative to Bank Cards for Expenses

Per Diem Rates Table 2026 for Germany and International Travel

/Listing%20Images/The%20rise%20of%20AI%20+%20ML_Listing%20Image.png)

8 Key Things to Consider Before Adopting an Expense Solution in 2026

/Listing%20Images/Higher%20Tax-Free%20Mileage%20Allowance%20From%202023%20in%20the%20Netherlands%20%E2%80%93%201.png)